The Secondary Market

American institutional lenders commonly fund two types of real estate loans: conventional, and government-insured and/or guaranteed, primarily by the Federal Housing Administration (HUD), the Veterans Administration (VA) and the Farmers Home Administration (FmHa). While lenders may choose to keep loans in their portfolios, the vast majority do not do so. They sell them to two government sponsored enterprises, the Federal National Mortgage Association, (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac), and to private-label companies set up by investment banks, pension funds, insurance companies, mutual funds and hedge funds. Ginnie Mae, a wholly-owned government corporation within the Department of Housing and Urban Development (HUD) guarantees –but does not buy- loans. Collectively, the system is known as the secondary market, an indispensable mechanism that continuously supplies lenders with working capital to fund more loans.

Historical Events

In September of 2008 Fannie and Freddie were seized by the Federal Housing Finance Agency as souring loans pushed them to the brink of insolvency; as a result, the government assumed the liability for their portfolio of loan guarantees. All said and done, the government now bears the risk for 90% of the nation’s $10 trillion mortgage market. Needless to say, in view of the magnitude of its chronic budget deficits and accumulated debt, it’s difficult to imagine how it could possibly make good on these guarantees should real estate prices collapse yet again.

Prior to the crash, investors worldwide viewed American real estate as a very low risk, profitable opportunity, and private capital flowed in from every corner of the world to satisfy the nation’s insatiable demand. The debacle changed that perception, and the supply of new money dwindled to an insignificant trickle. To compensate for the shortfall, which threatened to push interest rates up and plunge the country into a full blown depression, the Federal Reserve (the Fed) reduced its target federal funds rate to near zero and expanded the holdings of longer term securities in its portfolio, the System of Open Market Account (SOMA), to include large-scale purchases of fixed-rate, mortgage backed securities (MBS). SOMA operations, the Fed’s primary means to implement monetary policy, are granted under Section 14 of the Federal Reserve Act and take place at the Trading Desk at the Federal Reserve Bank of New York (FRBNY) exclusively with primary dealers (banks and security brokerages) that the FRBNY has selected for its operations. The Fed’s purchase program began in November 2008. By August 14, 2013 it held $1.264 trillion in MBS and $1.998 trillion in U.S. Treasury securities bills. Essentially the Fed has used its unique authority to create money as it sees fit to replace the $3.262 trillion capital shortfall caused by the collapse. This is an open-ended program, to be continued until the Fed feels that the economy has improved sufficiently. Left unanswered is the question of how much interest rates would rise and how that would affect real estate prices.

Outlook

There’s nothing to indicate that private capital will return to fund loans any time soon on a scale comparable to pre-2008. In fact, there’s a host of reasons why institutional lenders and private investors are reluctant to lend without government guarantees. To begin with, they expect to earn fees for making mortgages that they sell to Fannie and Freddie and to generate income while placing the risk on the government’s balance sheet. In addition, deep flaws remain in the mortgage securitization process, particularly with respect to the lack of transparency in privately issued securities. For example, although the banks issuing the securities do provide some data like borrowers’ incomes and credit scores, investors are not granted access to the actual loan files to determine if the type and quality of the loans meet their investment standards. Another powerful reason is the continuing impoverishment of the middle class, now afflicting roughly half of the population and with no relief in sight. Furthermore, nonexistent job security, declining benefits, and the skyrocketing cost of medical care and college student debt (the latter, by the way, does not guarantee a job), collectively suggest a higher probability that at some point in the future borrowers may be unable to make payments on mortgages they take out today. Add to that chronic political gridlock, which threatens to dissolve what’s left of the glue holding the nation together, and it’s not difficult to understand big money’s reluctance to lend.

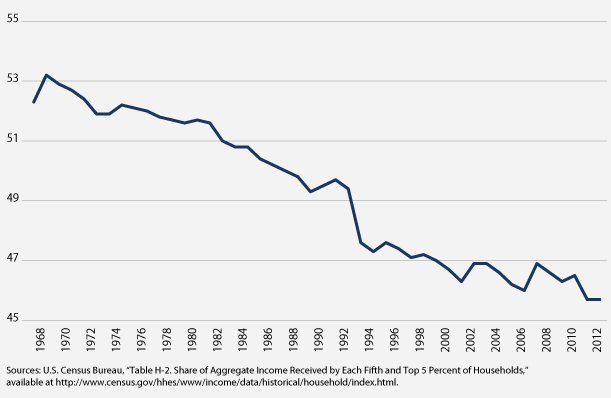

The Truth

The widening gap in the distribution of income and wealth is the reason for the middle classes’ declining standard of living. The 400 richest Americans own more wealth than the bottom 150 million put together, and the richest 1% own more than 35% of the country’s wealth; in contrast, the bottom 50% control just 2.5%. And the trend is accelerating. Since the official end of the recession in 2009, income for the bottom 99% grew by 4%; in contrast, for the top 1% it grew by 31%.

Middle Class Income

This situation has ominous implications for the U.S., nominally still the world’s largest economy and therefore with the most to lose. It is a historical fact that when societies get too unequal bad things happen. They become inefficient, stagnant, subject to social/civil/ethnic unrest and unable to compete for long with rising powers that eventually overpower them. While this extreme inequality could be reduced somewhat by tangential administrative and regulatory changes such as increasing investment in education and reforming the entire tax system, the overall trend will not be halted –much less reversed- until the root cause of the problem is formally acknowledged, confronted and addressed: unlike the upper class, the working and middle classes cannot tap directly into the great fountain of wealth emanating from China’s growth. As we shall see, this could be corrected without resorting to a redistribution of current wealth.

Consequences

The growing impoverishment of the middle class has caused a corresponding decline in the real estate index of affordability –the number of people who can afford to buy at current prices. Although the demand for housing has not declined, generally the construction industry has catered to the upper class simply because profit margins are higher and there are more qualified buyers. Understandably, due to its declining purchasing power, virtually no new housing is being built for the middle class; unable to buy, people are being forced to pay ever higher rents or to live with others. In effect, the middle class is being squeezed by declining incomes on the one hand and higher housing, medical and education costs on the other, and there’s no relief in sight.

As mentioned earlier, this trend cannot be halted –much less reversed- solely by tangential measures such as tax reform and by expanding the number of college graduates. The former cannot make up for the loss of millions of well-paying middle class jobs, and the latter is a fallacy to the extent that our colleges and universities don’t have the capacity to accept everyone who would like to attend. In fact, even if universities were completely free and staffed with enough professors and classrooms to accommodate every high school graduate without any restrictions or conditions, the country would still need farm laborers, electricians, plumbers and carpenters. None of these occupations require a degree, but they all need to make living wages. No, only a specific, feasible project designed to create thousands –if not millions- of high paying, permanent middle class jobs that cannot be outsourced or relocated will do, and new construction will be a fundamental part of it.

New Tracts, Towns, Cities

The construction portion of this proposal is a natural complement to the proposed parallel economy in the desert. But these new tracts, towns and cities would be unlike any others ever built. Each and every building –residential, commercial or industrial- would be equipped with the latest solar capturing technology (newly discovered materials and techniques have pushed the efficiency rate to 44.7%) designed to generate a surplus of electricity. Homes would be equipped with batteries to be charged during the day and used at night, when demand is lower. The rest of the surplus electricity would be transmitted to hydrogen and water plants via a private local grid that would not be connected to the existing state grid. Each homeowner would be free to install as many solar panels –within safety, practical and aesthetic limits- to generate as much electricity as desired to be sold at market rates. A portion of the profit from the sale of the hydrogen and water would be allocated to amortize the debt incurred to build the macro infrastructure, including the canal and lakes; the rest would be distributed among the homeowners according to a formula designed to reward and thus encourage maximum production of electricity. The funds would be deposited in escrow accounts for each property; a fee would be deducted for the maintenance and repair of the private grid –which would be done by licensed contractors who would bid every few years- and of the generating equipment in each home. The rest would be used to help pay the monthly payment on each property’s first mortgage, property taxes or insurance. If there is any money left, it would be distributed to the property owners. To protect homeowners, their right to generate electricity using solar energy should be non-transferable and be appurtenant to the land. To qualify for profit sharing from the hydrogen, water and electricity produced by those plants, which would be owned exclusively by property owners supplying them with power, residences should be owner-occupied. Of course, all real estate would be bought and sold in the open market as it normally is.

These new income streams would lower the risk of future default on purchase money loans and encourage private capital to participate without government guarantees. More importantly, a direct link would be established between middle class homeowners in the U.S. and hydrogen consumers in China, India and other similar markets. Currently this is the exclusive domain of shareholders of multinational corporations and wealthy investors.

Getting Started

There are two phases to this project. The first entails construction of the macro infrastructure –the canal, saltwater lakes, plants (hydrogen, hydro (gravity) and water), homes and supporting businesses in Death Valley. The second phase would see the expansion to suitable areas throughout the southwest and the introduction of secondary businesses such as recreation, agriculture and fish farming.

Financing

There are several ways to finance the macro infrastructure portion of project. One could be to create a special entity similar to the Tennessee Valley Authority, but with key differences. It would issue bonds that the Federal Reserve would buy, secured by the income derived from the sale of surplus electricity, manufactured water, hydrogen, and a lien on the instantaneous appreciation that would occur as the vacant, dry land is transformed into a thriving new economy. Better yet, no new taxes would be required, and since the Fed has considerable latitude to act without the approval of the Legislative and/or Executive branches of government, it might be possible to bypass political gridlock.

Another way to increase upfront revenue would be to require clients –countries or states that need clean water and hydrogen- to pay annually a priority fee to guarantee a portion of the hydrogen produced.

Conclusion

Overall, this should meet the fundamental demands of the left: millions of long-term, well-paid jobs that cannot be outsourced or relocated, significant reduction of the unemployed and underemployed, and higher tax revenue from a dramatic expansion of the tax base rather than from higher tax rates; and of the right: reduced federal spending on entitlements (more people would be working) and no new taxes or higher tax rates. The ripple effect of an additional economy on this scale would benefit the entire country. The environment would improve worldwide as hydrogen powered plants replace fossil fuels to generate electricity –natural gas could be diverted to replace gasoline as the fuel of choice for vehicles- and to simultaneously manufacture clean water wherever they may be built, even in the middle of the driest deserts. Existing big businesses would benefit from a revitalized purchasing power of the American middle class, and farmers would enjoy a reliable, predictable, permanent new source of water and fertilizers completely independent of the rain/precipitation cycle and thus impervious to drought.